CONVENTIONAL PLAYBOOK

Research

All Standard Disclaimers Apply & Seller Rights Retained

UNCONVENTIONALLY CONVENTIONAL!

July 2025, 90-Page Report

LOWER 48 ONSHORE VERTICAL

Seven U.S. Regions

M&A, E&P, Capital Markets

Total: 13.4 Bcfpd & 1.2 MMBopd

Privates: 9.3 Bdfpd & 633 MBopd

Publics: 4.1 Bcfpd & 533 MBopd

~10,000 Private Operators

Just ~1,300 Privates produce >100 Boepd

Top 35 Privates - 12 are Family Owned

Quantum & Kayne Anderson Active in P/E

San Andres, Strawn, Yeso Next Wave

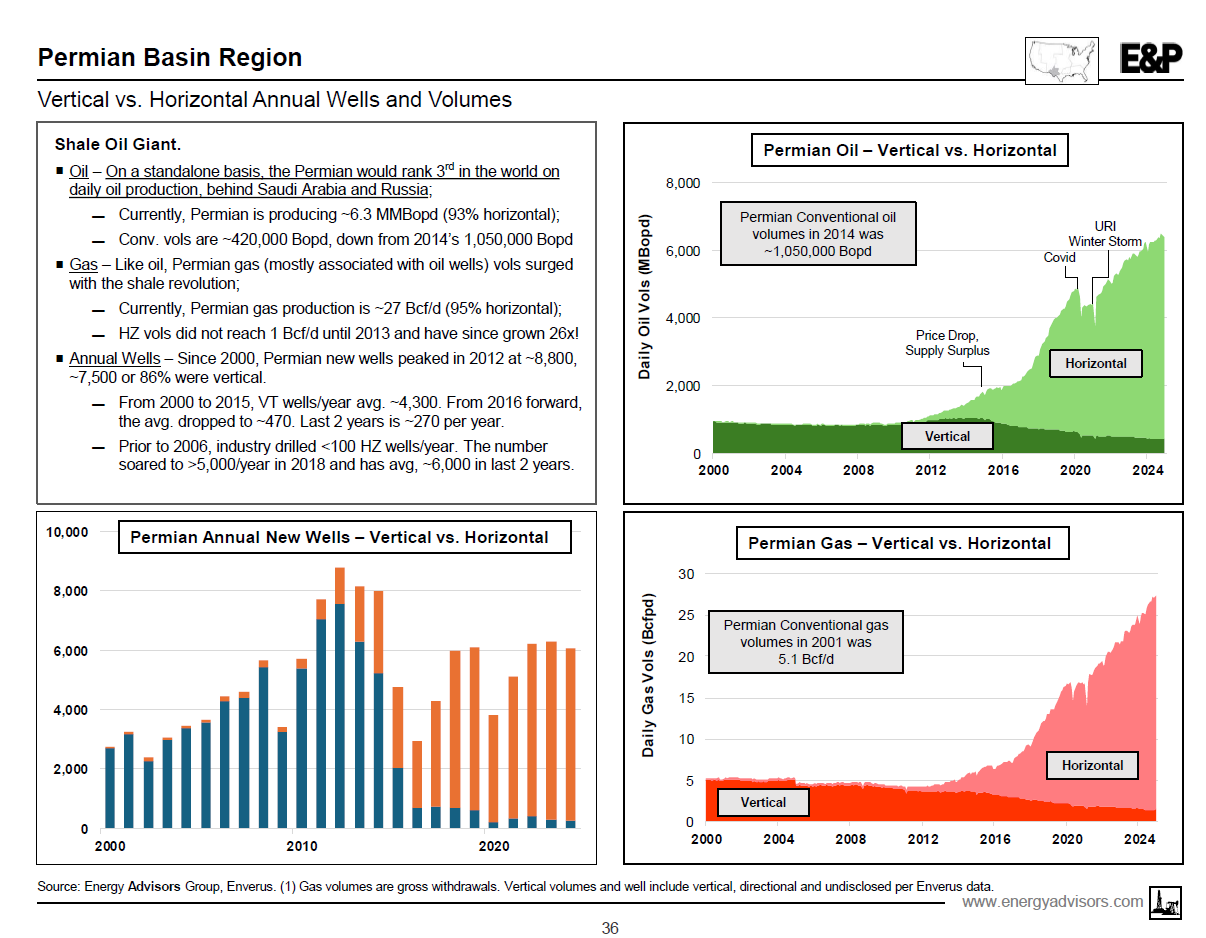

Permian takes 36% of oil volumes

Rockies take 51% of gas volumes

LOGIN TO DOWNLOAD FULL 90-PG STUDY

RS 2507RG

Energy Advisors Group has released our Lower 48 Onshore Conventional Study as a continuation of our Market Monitor Series and thought leadership efforts. This inaugural 90-page Special Report drills down on Lower 48 onshore conventional E&P (vertical & directional wells). We provide fresh perspectives on M&A, E&P, and Capital Markets.

The study takes a deep dive into public vs private conventional activity and dissects the data by U.S. regions. We also touch on hot topics like the rising use of ABS financing for conventional PDP, the application of shale tech (horizontal precise targeting in conventional reservoirs), and the existence of conventional buried treasures (moderate risk/high impact prospects) as capital fled to back shale resource development.

Here are our quick quotes and takeaways from our report.

Quick Quotes:

-------Future? “The shift in onshore volumes from conventional to unconventional is remarkable and historic. Conventional onshore production has declined over 50% since 2014 to ~1.2 MMbopd & ~13.4 Bcf/d. So, what does the future hold?"

-------Increasing A&D?. “While conventional M&A traditionally makes up only 6-8% of deal value over the last 5-8 years, recent transactions from Hilcorp and Diversified and now Mach are driving a decent amount of aggregation.”

-------Outlook. “Owners of low-decline PDP assets can tap ready buyers including local operators and financial players. These conventional assets are attractive as they provide steady cash flow and potential upside with 'shale tech'."

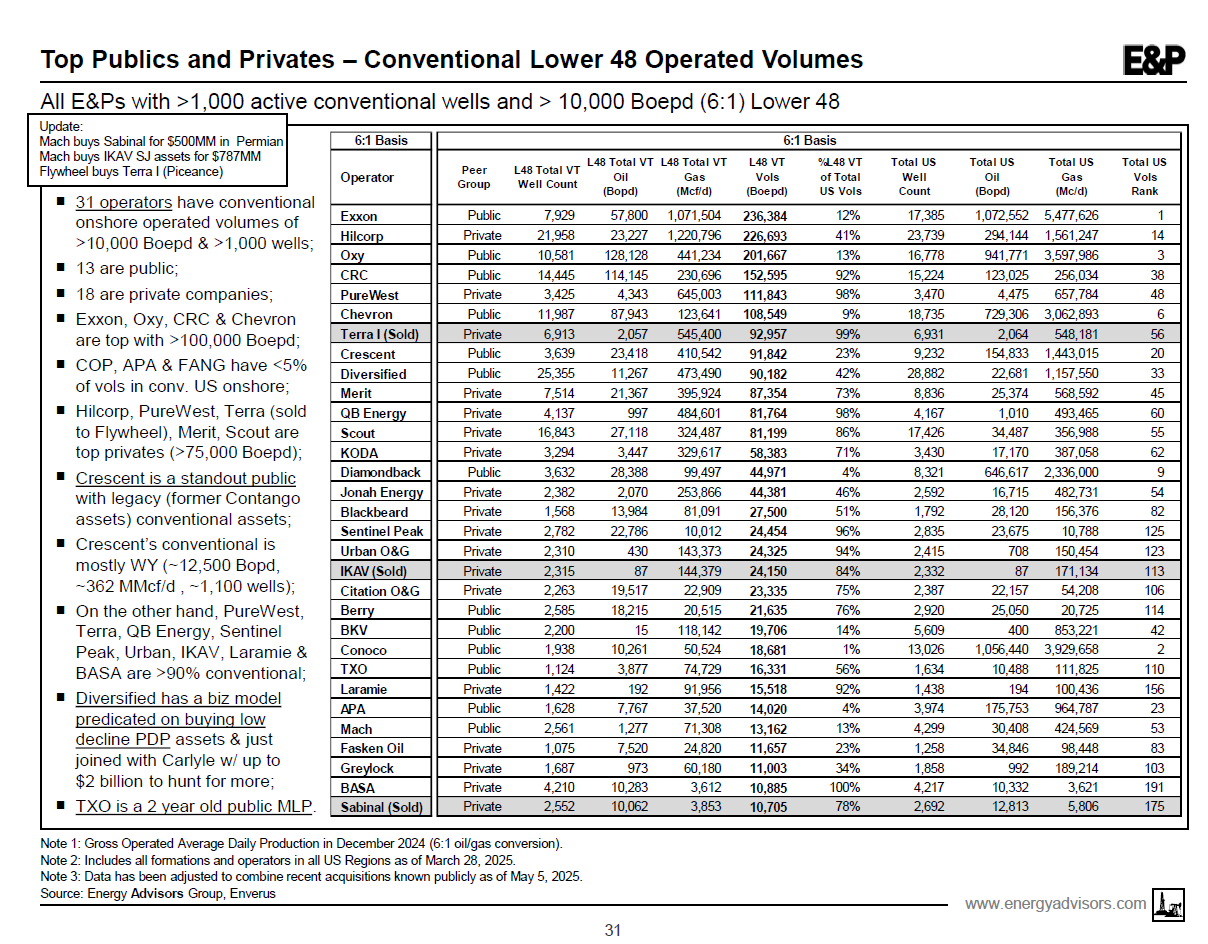

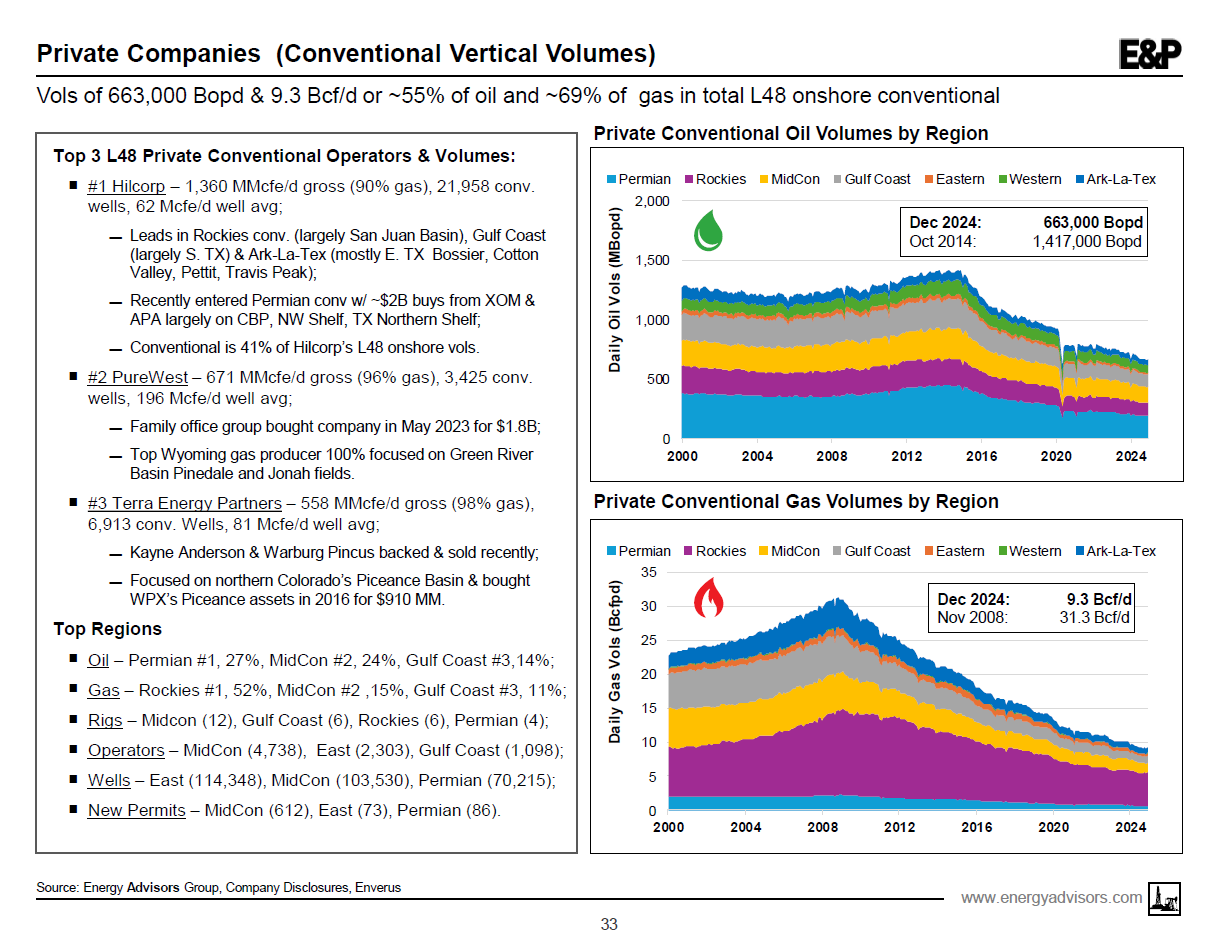

-------Privates. “Out of ~11,000 private operators with conventional production onshore, ~1,500 produce daily volumes >100 Boepd. Hilcorp leads. The Rockies is home to the next two largest conventional operators, PureWest and Terra I (which was recently sold to Flywheel)."

-------Regions. “The Permian leads all regions for onshore conventional oil volumes with 27%. Blackbeard is the region’s top conventional private. The Rockies leads for conventional gas volumes with 52%. Hilcorp leads the region with assets in the San Juan Basin."

-------Capital. “Recent deals are all about mature PDP w/low decline, who’s predictive reserves can be hedged and aggressively financed. Diversified & Carlyle have $2B to hunt for more PDP in a 'highly attractive market'."

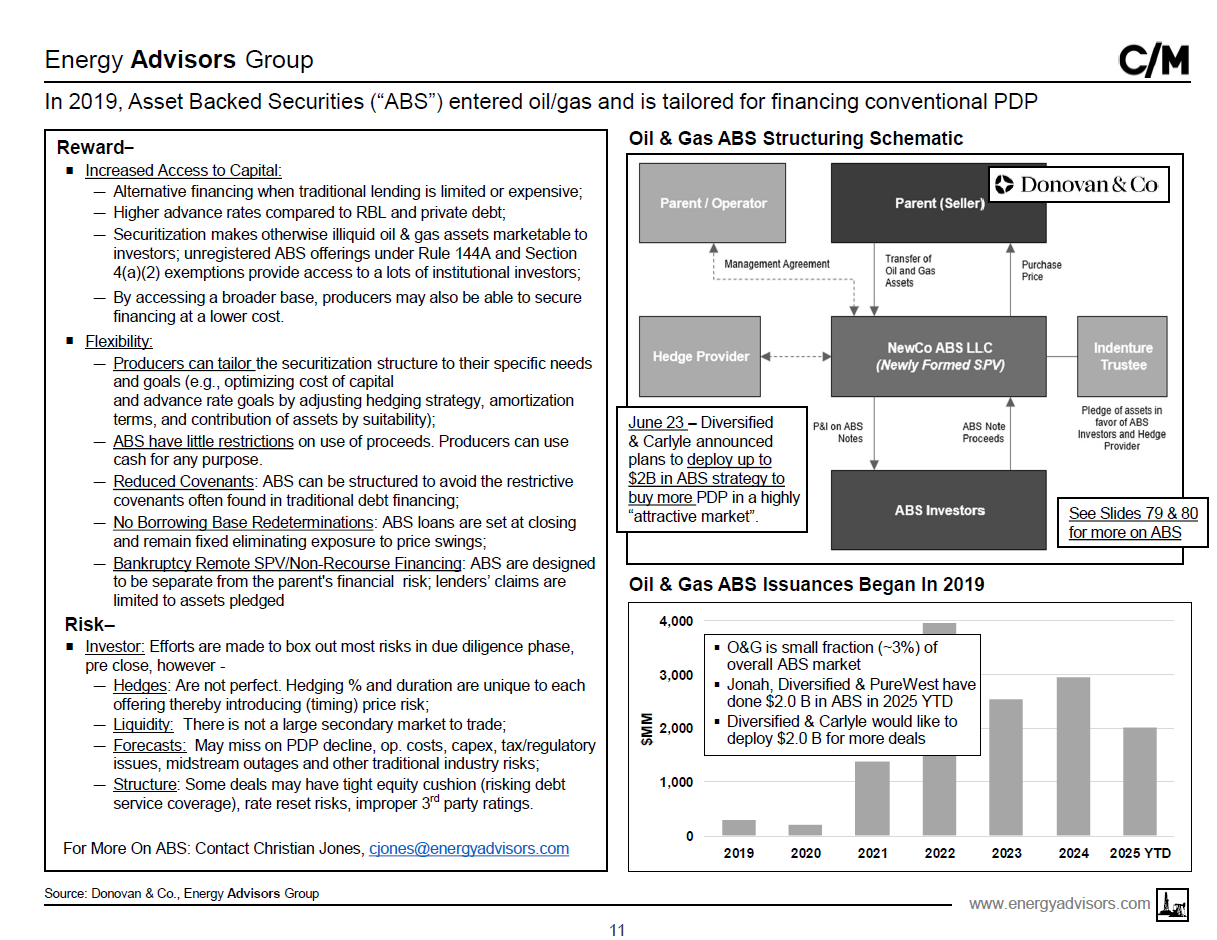

-------ABS. “Conventional PDP is tailor made for ABS. Key criteria include lots of wells, low decline rate and ability to hedge – all designed to reduce concentration and price risk. Operators can use proceeds for any purposes."

-------Next Wave! “Permian’s CBP and NW Shelf assets are held by lots of publics and privates. Expect more consolidation amid a growing wave of horizontal redevelopment that is underway.”

Quick Key Takeaways---

A&D – PDP with Upside. Is there room for more consolidation?!

- Since 2022, conventional deals represent ~7% of U.S. A&D market or an average of $1.9 billion per quarter;

- Hilcorp entered the Permian buying legacy assets from APA ($950MM) and Exxon ($1.5B);

- Diversified Energy has aggressively bought conventional assets in the Anadarko, Ark-La-Tex & Appalachia and recently secured additional capital from Carlyle;

- Mach Natural Resources accelerated its conventional strategy entering San Juan and Permian & doubling vols;

- Williams recently bought more upstream gas in the Green River to integrate with midstream assets;

- Terra Energy I (Kayne Anderson & Warburg) sold ~560 MMcfe/d (Piceance) to Flywheel and rebooted;

- Burk Royalty quietly bought NGP-backed Steward Energy II building on its San Andres HZ book;

- Looking forward, we expect larger publics to continue shedding conventional assets as well as some privates.

E&P – The Privates, obviously, lead in vertical drilling. Is the next growth wave HZ drilling in conv. plays?

- L48 onshore conventional volumes account for ~9% & ~12% of US oil & gas volumes, respectively;

- Permian leads in conventional oil while the Rockies dominate conventional gas volumes;

- 31 operators have onshore conventional volumes of >10,000 Boepd and >1,000 wells (13 public, 18 private);

- Crescent Energy is a standout with material conventional vols after its pivot to Eagle Ford’s #3 operator by net volumes – market is reporting that CRGY has a process underway to sell some legacy assets;

- Private companies have drilled ~80% of new conventional wells since 2020;

- These same privates control ~70% of conventional gas volumes and ~55% of conventional oil;

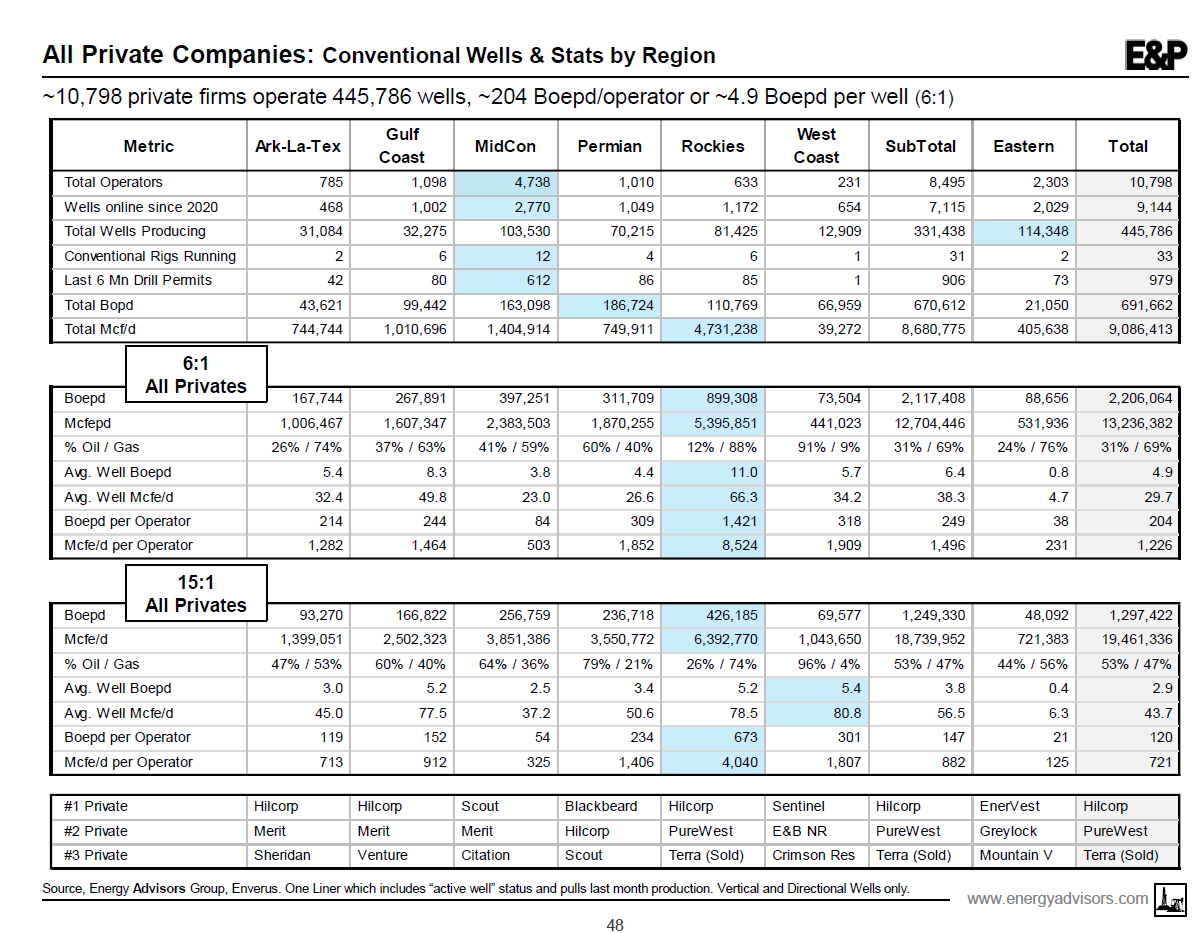

- There are nearly 11,000 privates of which ~85% are small and producing <100 Boepd;

- About 1,500 privates (>100 Boepd) control ~60% of conventional vols, Top 35 control ~33%;

- Blackbeard is the most active conventional driller since 2020 – drilling 9 wells/month in Winkler, Crane, Cos., on the Permian’s Central Basin Platform (CBP) (avg: 6,050’ TVD, peak 150 Bopd, 690 Mcf/d);

- Shale tech can be applied to conventional reservoirs and lead to another wave of innovation;

- Technologies incl. precise hz steering; multi-pad development; multi-well simultaneous stimulation; remote monitoring; stacked-pay co-development and more;

- Permian operators are applying shale tech to conventional reservoirs like the San Andres, Strawn and Yeso.

Capital Markets – What capital is driving conventional players? What is ABS?

- Conventional players: (a) Family (e.g., Hilcorp, Citation, Fasken), (b) Operators w/private capital, institutional investors (e.g., Merit, Scout, Jonah) and (c) traditional P/E (e.g., Quantum, Kayne Anderson, NGP);

- Asset backed securities (ABS) is a rising star for low decline mature PDP for financing;

- Diversified strikes deal w/Carlyle to pursue up to $2 B in PDP in a “highly compelling” market;

- Kayne Anderson re-ups with $300 MM for Terra II team to go buy conventional again and $400 MM with ex-Flywheel execs for Newco South Wind E&P. In May 2025, Kayne closed its largest fund w/$2.25 B;

- High Net Worth & Family Offices increasingly taking first chair on funding running “P/E like” strategies.

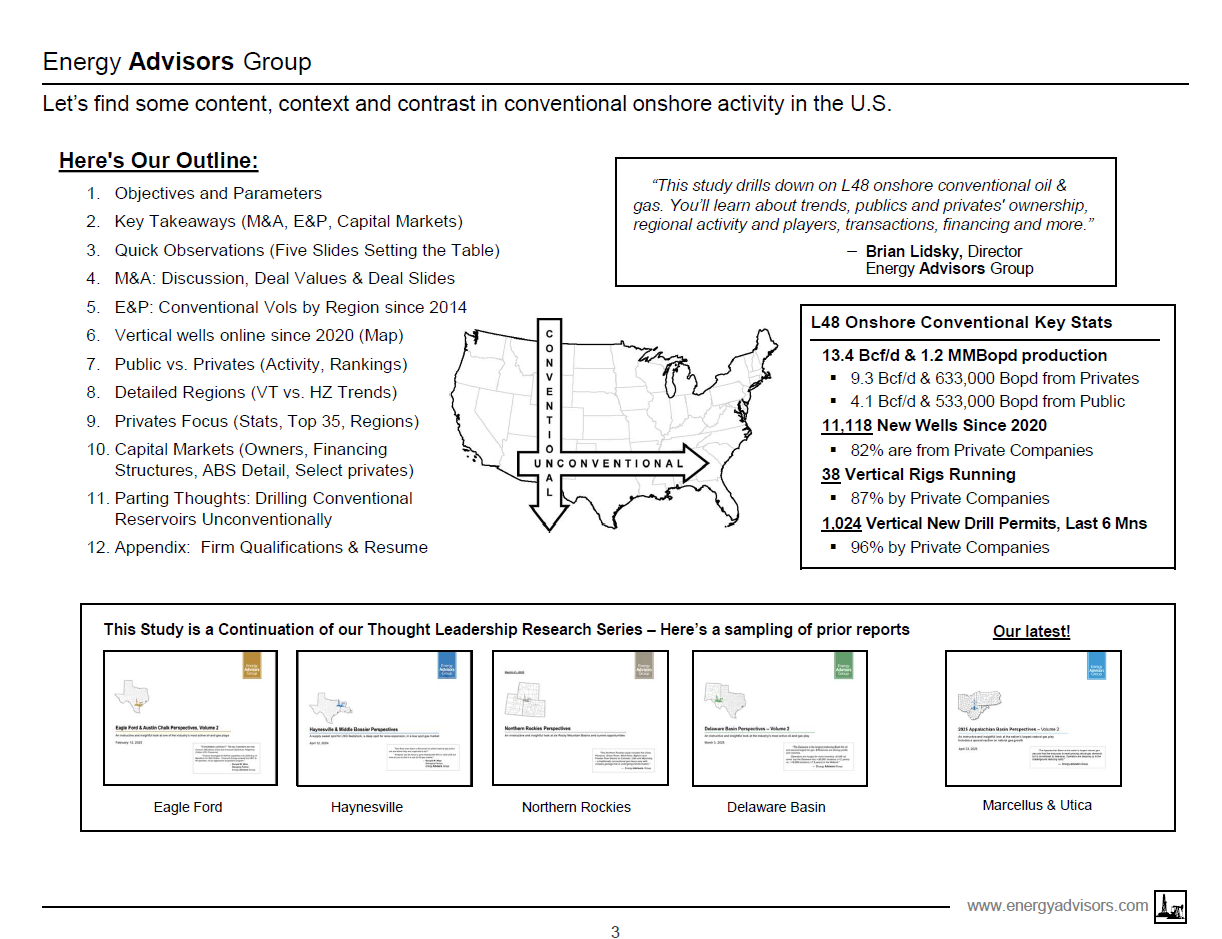

Here is the Outline and some Quick Key Stats ---

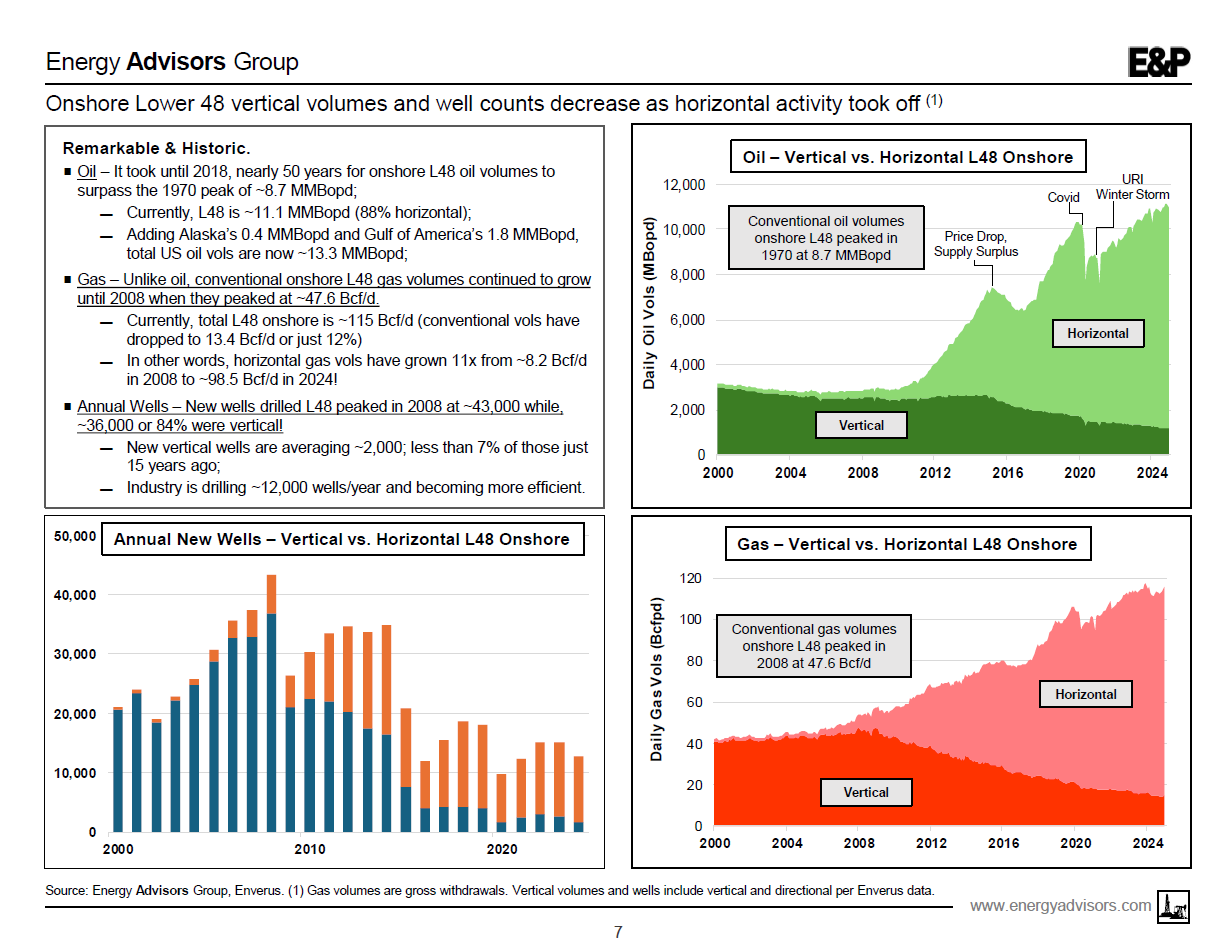

Here's an overview of L48 Onshore oil & gas volumes and drilling (VT v. HZ) since 2000 ---

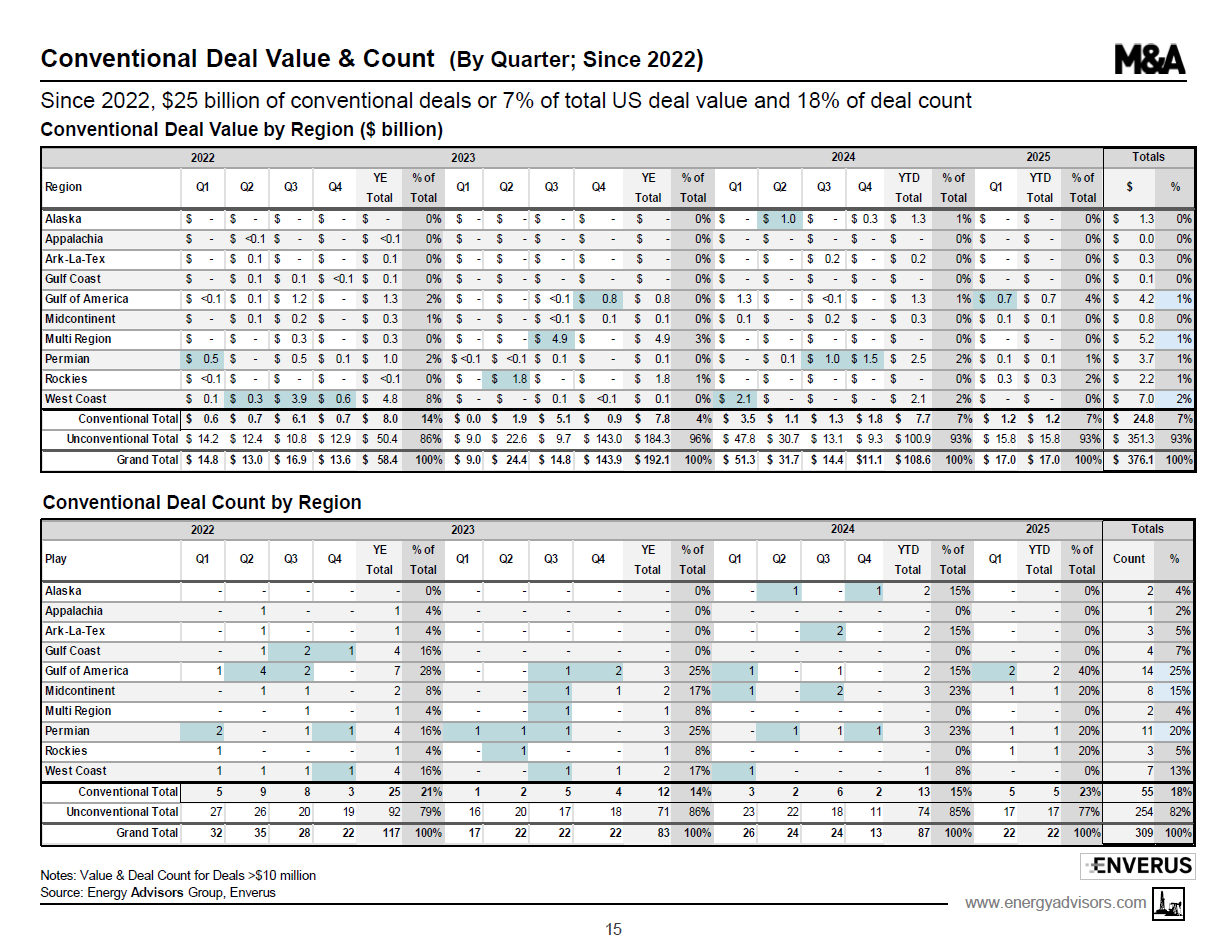

Since 2022, conventional transactions are ~7% of the total U.S. ---

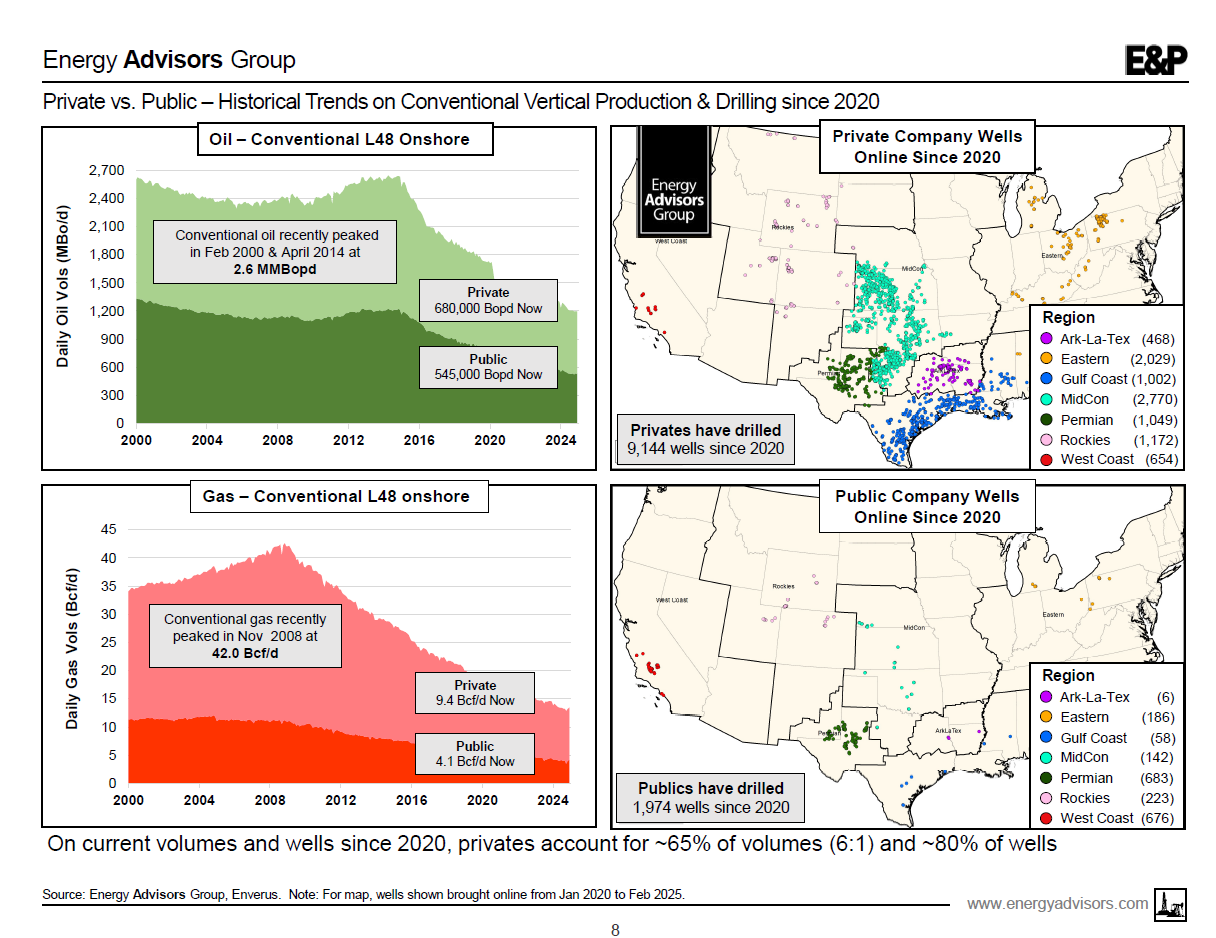

Here's an overview of Public v. Private in conventional activity by U.S. Regions (Privates Dominate) ---

This slide ranks ALL E&Ps (public & private) w/ conventional volumes > 10,000 Boepd & >1,000 active wells ---

Here are 3 slides from our deep dive of Private E&Ps --- This 1st slide shows Private E&P's Vols by Region ---

This 2nd slide on Private E&Ps counts operators (~11,000), wells, volumes (6:1 & 15:1), permits by Region ---

This 3rd slide on Private E&P's is an example of the opening slide on the Permian Region ---

Here's a slide showing ABS financing is growing as an alternative financing for PDP ---

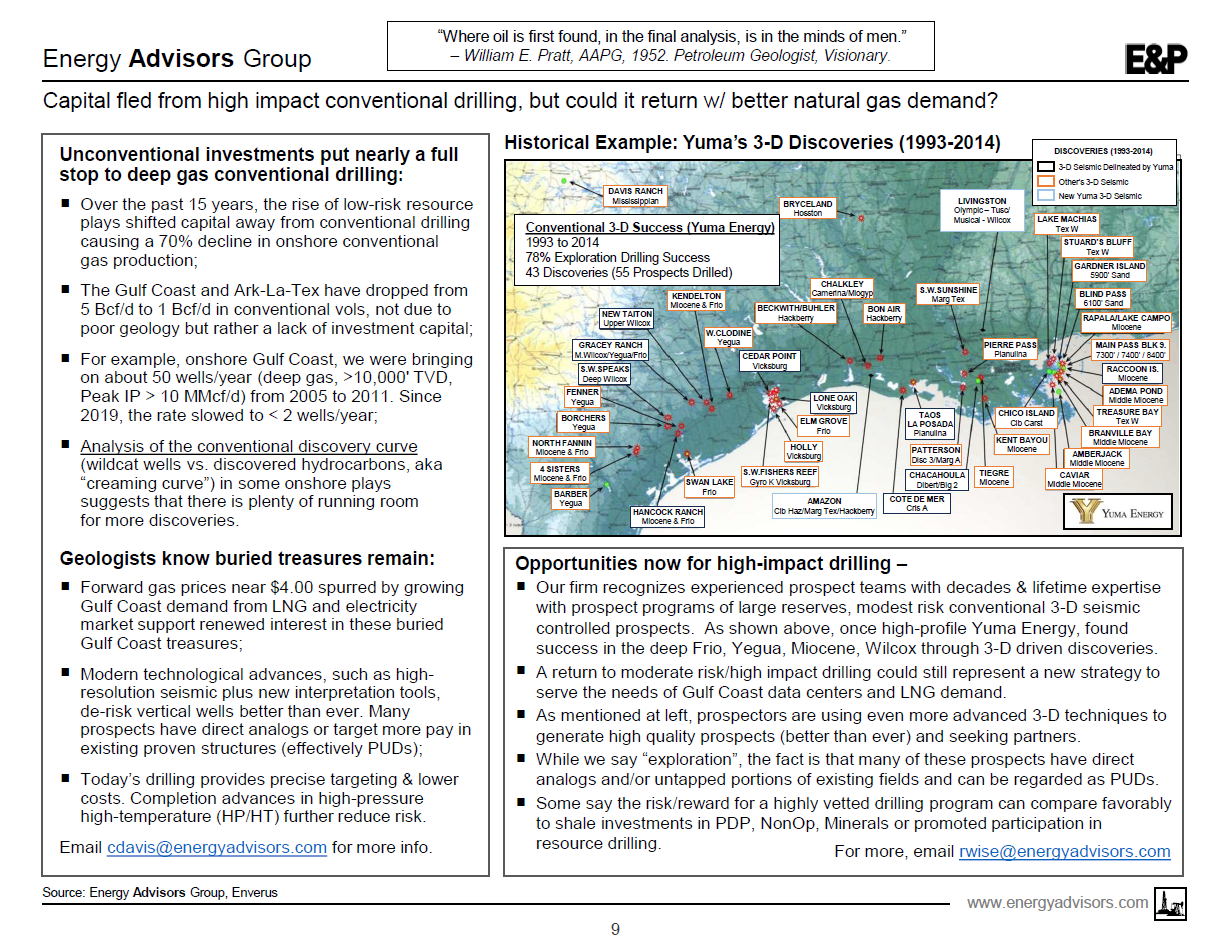

We recognize that traditional High-Impact conventional prospect programs are an Opportunity Now ---

The above slides are just a small portion of the full report which is available to the right. This is a timely report as E&Ps like Diversified and Mach Natural Resources are aggressively pursuing conventional PDP. These legacy assets are also contributing to a growing redevelopment wave as operators deploy horizontal drilling in conventional reservoirs (examples are formations like the San Andres and Yeso in the Permian). While not as blanket as a traditional shale plays, some conventional reservoirs have plenty of oil and gas remaining even after a first vertical development wave. Remember early on when the Spraberry and Middle Bakken were delivering strong results from vertical drilling.

Our firm is ready to assist owners of conventional assets in a competitive divestment process and to help buyers find more quality conventional PDP assets for their portfolio. Call or email us for a private consultation.

TO LEARN MORE:

Blake Dornak

Vice President

Phone: 713-600-0169

---Email: [email protected]

Brian Lidsky

Director

Phone: 713-600-0138

---Email: [email protected]

-----------------------------------------------------

IF YOU NEED ASSISTANCE downloading the full report or creating a login into our platform , contact:

Blake Dornak

Vice President

Phone: 713-600-0169

– Email: [email protected]

Our firm has been serving the needs of buyers, sellers and capital providers for over thirty-five years.

UNCONVENTIONALLY CONVENTIONAL!

July 2025, 90-Page Report

LOWER 48 ONSHORE VERTICAL

Seven U.S. Regions

M&A, E&P, Capital Markets

Total: 13.4 Bcfpd & 1.2 MMBopd

Privates: 9.3 Bdfpd & 633 MBopd

Publics: 4.1 Bcfpd & 533 MBopd

~10,000 Private Operators

Just ~1,300 Privates produce >100 Boepd

Top 35 Privates - 12 are Family Owned

Quantum & Kayne Anderson Active in P/E

San Andres, Strawn, Yeso Next Wave

Permian takes 36% of oil volumes

Rockies take 51% of gas volumes

LOGIN TO DOWNLOAD FULL 90-PG STUDY

RS 2507RG

Energy Advisors Group has released our Lower 48 Onshore Conventional Study as a continuation of our Market Monitor Series and thought leadership efforts. This inaugural 90-page Special Report drills down on Lower 48 onshore conventional E&P (vertical & directional wells). We provide fresh perspectives on M&A, E&P, and Capital Markets.

The study takes a deep dive into public vs private conventional activity and dissects the data by U.S. regions. We also touch on hot topics like the rising use of ABS financing for conventional PDP, the application of shale tech (horizontal precise targeting in conventional reservoirs), and the existence of conventional buried treasures (moderate risk/high impact prospects) as capital fled to back shale resource development.

Here are our quick quotes and takeaways from our report.

Quick Quotes:

-------Future? “The shift in onshore volumes from conventional to unconventional is remarkable and historic. Conventional onshore production has declined over 50% since 2014 to ~1.2 MMbopd & ~13.4 Bcf/d. So, what does the future hold?"

-------Increasing A&D?. “While conventional M&A traditionally makes up only 6-8% of deal value over the last 5-8 years, recent transactions from Hilcorp and Diversified and now Mach are driving a decent amount of aggregation.”

-------Outlook. “Owners of low-decline PDP assets can tap ready buyers including local operators and financial players. These conventional assets are attractive as they provide steady cash flow and potential upside with 'shale tech'."

-------Privates. “Out of ~11,000 private operators with conventional production onshore, ~1,500 produce daily volumes >100 Boepd. Hilcorp leads. The Rockies is home to the next two largest conventional operators, PureWest and Terra I (which was recently sold to Flywheel)."

-------Regions. “The Permian leads all regions for onshore conventional oil volumes with 27%. Blackbeard is the region’s top conventional private. The Rockies leads for conventional gas volumes with 52%. Hilcorp leads the region with assets in the San Juan Basin."

-------Capital. “Recent deals are all about mature PDP w/low decline, who’s predictive reserves can be hedged and aggressively financed. Diversified & Carlyle have $2B to hunt for more PDP in a 'highly attractive market'."

-------ABS. “Conventional PDP is tailor made for ABS. Key criteria include lots of wells, low decline rate and ability to hedge – all designed to reduce concentration and price risk. Operators can use proceeds for any purposes."

-------Next Wave! “Permian’s CBP and NW Shelf assets are held by lots of publics and privates. Expect more consolidation amid a growing wave of horizontal redevelopment that is underway.”

Quick Key Takeaways---

A&D – PDP with Upside. Is there room for more consolidation?!

- Since 2022, conventional deals represent ~7% of U.S. A&D market or an average of $1.9 billion per quarter;

- Hilcorp entered the Permian buying legacy assets from APA ($950MM) and Exxon ($1.5B);

- Diversified Energy has aggressively bought conventional assets in the Anadarko, Ark-La-Tex & Appalachia and recently secured additional capital from Carlyle;

- Mach Natural Resources accelerated its conventional strategy entering San Juan and Permian & doubling vols;

- Williams recently bought more upstream gas in the Green River to integrate with midstream assets;

- Terra Energy I (Kayne Anderson & Warburg) sold ~560 MMcfe/d (Piceance) to Flywheel and rebooted;

- Burk Royalty quietly bought NGP-backed Steward Energy II building on its San Andres HZ book;

- Looking forward, we expect larger publics to continue shedding conventional assets as well as some privates.

E&P – The Privates, obviously, lead in vertical drilling. Is the next growth wave HZ drilling in conv. plays?

- L48 onshore conventional volumes account for ~9% & ~12% of US oil & gas volumes, respectively;

- Permian leads in conventional oil while the Rockies dominate conventional gas volumes;

- 31 operators have onshore conventional volumes of >10,000 Boepd and >1,000 wells (13 public, 18 private);

- Crescent Energy is a standout with material conventional vols after its pivot to Eagle Ford’s #3 operator by net volumes – market is reporting that CRGY has a process underway to sell some legacy assets;

- Private companies have drilled ~80% of new conventional wells since 2020;

- These same privates control ~70% of conventional gas volumes and ~55% of conventional oil;

- There are nearly 11,000 privates of which ~85% are small and producing <100 Boepd;

- About 1,500 privates (>100 Boepd) control ~60% of conventional vols, Top 35 control ~33%;

- Blackbeard is the most active conventional driller since 2020 – drilling 9 wells/month in Winkler, Crane, Cos., on the Permian’s Central Basin Platform (CBP) (avg: 6,050’ TVD, peak 150 Bopd, 690 Mcf/d);

- Shale tech can be applied to conventional reservoirs and lead to another wave of innovation;

- Technologies incl. precise hz steering; multi-pad development; multi-well simultaneous stimulation; remote monitoring; stacked-pay co-development and more;

- Permian operators are applying shale tech to conventional reservoirs like the San Andres, Strawn and Yeso.

Capital Markets – What capital is driving conventional players? What is ABS?

- Conventional players: (a) Family (e.g., Hilcorp, Citation, Fasken), (b) Operators w/private capital, institutional investors (e.g., Merit, Scout, Jonah) and (c) traditional P/E (e.g., Quantum, Kayne Anderson, NGP);

- Asset backed securities (ABS) is a rising star for low decline mature PDP for financing;

- Diversified strikes deal w/Carlyle to pursue up to $2 B in PDP in a “highly compelling” market;

- Kayne Anderson re-ups with $300 MM for Terra II team to go buy conventional again and $400 MM with ex-Flywheel execs for Newco South Wind E&P. In May 2025, Kayne closed its largest fund w/$2.25 B;

- High Net Worth & Family Offices increasingly taking first chair on funding running “P/E like” strategies.

Here is the Outline and some Quick Key Stats ---

Here's an overview of L48 Onshore oil & gas volumes and drilling (VT v. HZ) since 2000 ---

Since 2022, conventional transactions are ~7% of the total U.S. ---

Here's an overview of Public v. Private in conventional activity by U.S. Regions (Privates Dominate) ---

This slide ranks ALL E&Ps (public & private) w/ conventional volumes > 10,000 Boepd & >1,000 active wells ---

Here are 3 slides from our deep dive of Private E&Ps --- This 1st slide shows Private E&P's Vols by Region ---

This 2nd slide on Private E&Ps counts operators (~11,000), wells, volumes (6:1 & 15:1), permits by Region ---

This 3rd slide on Private E&P's is an example of the opening slide on the Permian Region ---

Here's a slide showing ABS financing is growing as an alternative financing for PDP ---

We recognize that traditional High-Impact conventional prospect programs are an Opportunity Now ---

The above slides are just a small portion of the full report which is available to the right. This is a timely report as E&Ps like Diversified and Mach Natural Resources are aggressively pursuing conventional PDP. These legacy assets are also contributing to a growing redevelopment wave as operators deploy horizontal drilling in conventional reservoirs (examples are formations like the San Andres and Yeso in the Permian). While not as blanket as a traditional shale plays, some conventional reservoirs have plenty of oil and gas remaining even after a first vertical development wave. Remember early on when the Spraberry and Middle Bakken were delivering strong results from vertical drilling.

Our firm is ready to assist owners of conventional assets in a competitive divestment process and to help buyers find more quality conventional PDP assets for their portfolio. Call or email us for a private consultation.

TO LEARN MORE:

Blake Dornak

Vice President

Phone: 713-600-0169

---Email: [email protected]

Brian Lidsky

Director

Phone: 713-600-0138

---Email: [email protected]

-----------------------------------------------------

IF YOU NEED ASSISTANCE downloading the full report or creating a login into our platform , contact:

Blake Dornak

Vice President

Phone: 713-600-0169

– Email: [email protected]

Our firm has been serving the needs of buyers, sellers and capital providers for over thirty-five years.