DEAL ALERT (BAYTEX MAY SELL E/F)

Research/Study

All Standard Disclaimers Apply & Seller Rights Retained

- Energy Advisors Group")

SPECIAL REPORT (OCT 14, 2025)

Media Reporting BTE Exploring EF Sale

BAYTEX POTENTIAL EAGLE FORD EXIT

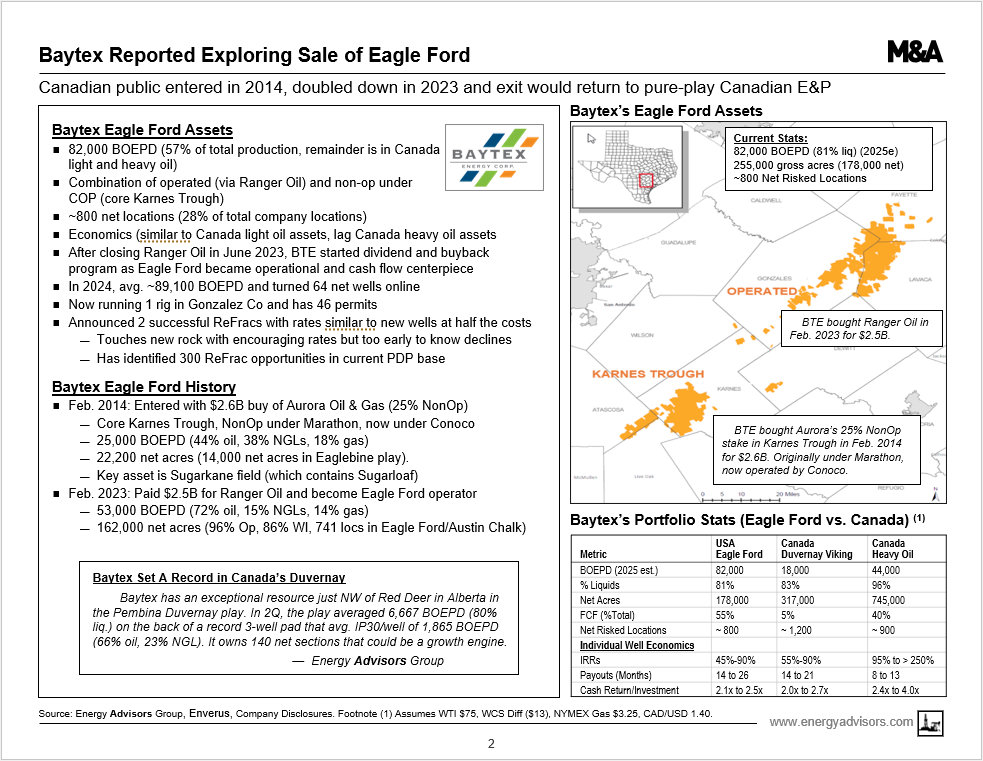

82,000 BOEPD (81% liquids)

178,000 Net Acres, 800 Risked Locations

Karnes Trough NonOp (Now Under COP)

And Op. via Ranger Oil Buy ($2.6B, 2023)

Sale Would Mark Return Home to Canada

Media Reports Up To $3B Potential Value

Sale Would Wipe Out All Debt, Strategy Shift

Baytex Ranks #11 Top Eagle Ford Operator

Baytex has Growth Pembina Duvernay

Also Cash Flow from Canada Heavy Oil

CLICK TO DOWNLOAD 7-PAGE REPORT

RS 2513DA

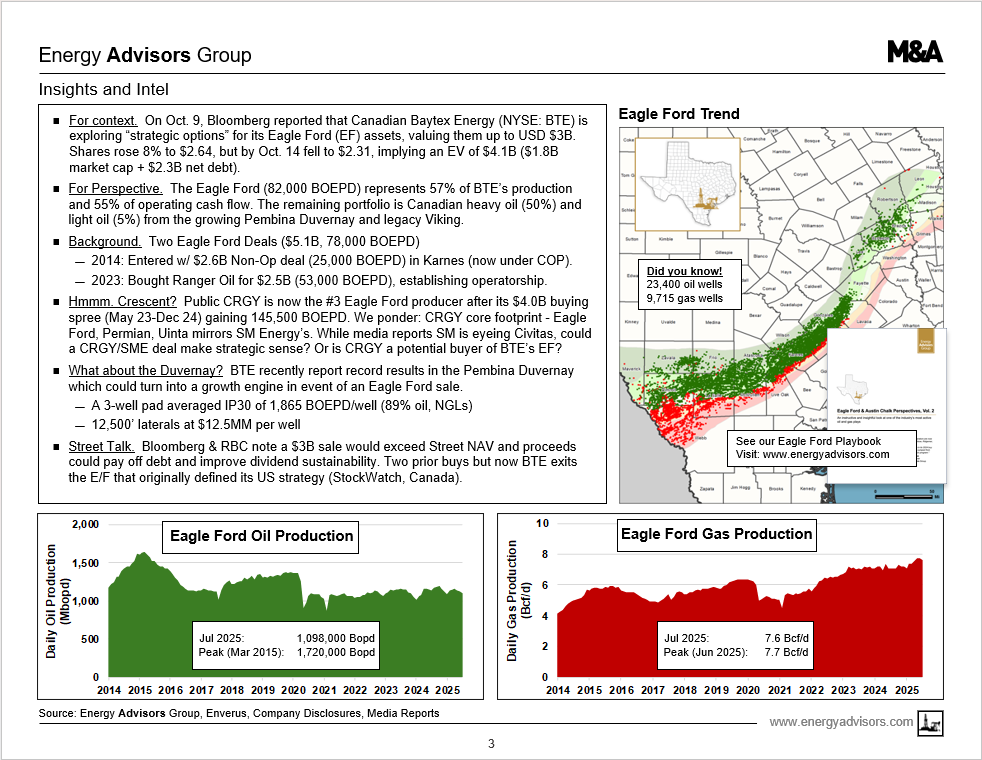

Energy Advisors Group (EAG) has issued a Deal Alert, Significant Deal on the Market, after media reports Baytex Energy is exploring a sale of its Eagle Ford assets for up to $3 billion.

A potential sale would mark a major strategic shift for Baytex back to Canada. Baytex entered the Eagle Ford in 2013 with a $2.6B NonOp purchase under Marathon at the time, now under COP, in the core Karnes Trough area. In 2023, Baytex began Eagle Ford operations with its $2.5B buy of Ranger Oil.

With an enterprise value of $4.1B as of October 14, 2025, a potential sale of up to $3 billion could clear BTE's $2.3B of net debt and allow the company to improve dividend sustainability. Also, it would allow a strategic shift to accelerate its Pembina Duvernay drilling for growth. In its 2Q report, Baytex announced record Pembina Duvernay IP30's of 1,865/BOEPD (89% oil, liquids) per well for a 3-well pad with 12,500' laterals and a $12.5 MM cost per well.

We note that Crescent Energy, now the Eagle Ford's #3 producer, paid $4.0 billion from May 2023 to December 2024 to buy 145,500 BOEPD in the Eagle Ford. Also, CRGY's core footprint - Eagle Ford, Permian and Uinta - mirrors that of SM Energy. While media is reporting SM Energy entertaining a merger with Civitas, could a Crescent + SM Energy deal make strategic sense. Or is Crescent Energy a potential buyer of Baytex's Eagle Ford assets.

Also, could the 25% NonOp under Conoco in the core Karnes Trough be bought independently given the strong market for NonOp now in a partial exit?

Baytex also recently achieved strong success with 2 Eagle Ford ReFracs that cost half that of a new well. The company believes the ReFrac touched new rock and it is too soon to determine the decline rate although Baytex is optimistic and has another 300 ReFrac opportunities in its existing PDP base.

Contents and Insights:

------ Baytex Eagle Ford Stats: 82,000 BOEPD est. 2025 net volumes, 255,000 gross acres (178,000 net), ~800 net risked locations, ~300 ReFrac opportunities, $680MM of 2025 CAPEX (57% of company total).

------ Deal History: Entered 2014 with $2.6B NonOp buy from Aurora Oil & Gas, now 25% WI under COP in Karnes Trough Area. In 2023, paid $2.5B for Ranger Oil establishing operations and gaining 53,000 BOEPD.

------ US v. Canada: Baytex's Eagle Ford operations account for 55% of total free cash flow and 57% of production.

------ Canada Base: Heavy oil in Peace River, Peavine, Lloydminster produces 44,000 BOEPD. Light oil in Viking (legacy) and Duvernay (growth) producing 18,000 BOEPD. Figures are 2025 full year estimates.

Here are our quick takeaways from our report along w/ two slides.

Quick Quotes:

------- Is it all about Canada? "Baytex has an exceptional resource just NW of Red Deer in Alberta in the Pembina Duvernay play. In 2Q, the play averaged 6,667 BOEPD (80% liq.) on the back of a record 3-well pad that avg. IP30/well of 1,865 BOEPD (66% oil, 23% NGL). It owns 140 net sections that could be a growth engine."

------- Content: “We rank and map the top 15 Eagle Ford operators (>85% of total volumes), provide a history of Eagle Ford deals >$100MM since May 2019, and graph total Eagle Ford oil and gas volumes since 2014."

------- Contrast: “Baytex's recent record success in its Pembina Duvernay play may be driving a potential Eagle Ford exit its Canadian assets may have a longer runway and better economics.”

------- Context: “An Eagle Ford exit would shrink Baytex's cash flow and volumes by more than half, although it would also return the company to a pure-play Canadian E&P and likely provide for more strategic options within Canada."

#1---

Here's an Overview

#2---

Here's our Insight & Intel on the Deal

The FULL 7-page report is available for download to the right.

Energy Advisors Group is working hard to expand our thought leadership leveraging our decades of industry expertise. We look forward to providing additional market insight for our clients through Market Monitor, Regional Perspectives, Deal Alerts and Quarterly M&A Outlook.

Our firm has been serving the needs of buyers, sellers and capital providers for over thirty-five years. We stand ready to assist asset owners in a competitive divestment process and to help buyers find off-market strategic assets for their portfolio. Call Rich Martin at 214-744-2495 or email rmartin@energyadvisors.com for a private consultation.

TO LEARN MORE:

Blake Dornak

Vice President

Phone: 713-600-0169

– Email: bdornak@energyadvisors.com

Brian Lidsky

Director-Research & Special Projects

Phone: 713-600-0138

– Email: blidsky@energyadvisors.com

IF YOU NEED ASSISTANCE downloading the full report or creating a login into our platform , contact:

Stephanie Epps

– Email: stephanie@energyadvisors.com

This article is for informational purposes only and not intended as financial advice. Please conduct your own research before investing.

SPECIAL REPORT (OCT 14, 2025)

Media Reporting BTE Exploring EF Sale

BAYTEX POTENTIAL EAGLE FORD EXIT

82,000 BOEPD (81% liquids)

178,000 Net Acres, 800 Risked Locations

Karnes Trough NonOp (Now Under COP)

And Op. via Ranger Oil Buy ($2.6B, 2023)

Sale Would Mark Return Home to Canada

Media Reports Up To $3B Potential Value

Sale Would Wipe Out All Debt, Strategy Shift

Baytex Ranks #11 Top Eagle Ford Operator

Baytex has Growth Pembina Duvernay

Also Cash Flow from Canada Heavy Oil

CLICK TO DOWNLOAD 7-PAGE REPORT

RS 2513DA

Energy Advisors Group (EAG) has issued a Deal Alert, Significant Deal on the Market, after media reports Baytex Energy is exploring a sale of its Eagle Ford assets for up to $3 billion.

A potential sale would mark a major strategic shift for Baytex back to Canada. Baytex entered the Eagle Ford in 2013 with a $2.6B NonOp purchase under Marathon at the time, now under COP, in the core Karnes Trough area. In 2023, Baytex began Eagle Ford operations with its $2.5B buy of Ranger Oil.

With an enterprise value of $4.1B as of October 14, 2025, a potential sale of up to $3 billion could clear BTE's $2.3B of net debt and allow the company to improve dividend sustainability. Also, it would allow a strategic shift to accelerate its Pembina Duvernay drilling for growth. In its 2Q report, Baytex announced record Pembina Duvernay IP30's of 1,865/BOEPD (89% oil, liquids) per well for a 3-well pad with 12,500' laterals and a $12.5 MM cost per well.

We note that Crescent Energy, now the Eagle Ford's #3 producer, paid $4.0 billion from May 2023 to December 2024 to buy 145,500 BOEPD in the Eagle Ford. Also, CRGY's core footprint - Eagle Ford, Permian and Uinta - mirrors that of SM Energy. While media is reporting SM Energy entertaining a merger with Civitas, could a Crescent + SM Energy deal make strategic sense. Or is Crescent Energy a potential buyer of Baytex's Eagle Ford assets.

Also, could the 25% NonOp under Conoco in the core Karnes Trough be bought independently given the strong market for NonOp now in a partial exit?

Baytex also recently achieved strong success with 2 Eagle Ford ReFracs that cost half that of a new well. The company believes the ReFrac touched new rock and it is too soon to determine the decline rate although Baytex is optimistic and has another 300 ReFrac opportunities in its existing PDP base.

Contents and Insights:

------ Baytex Eagle Ford Stats: 82,000 BOEPD est. 2025 net volumes, 255,000 gross acres (178,000 net), ~800 net risked locations, ~300 ReFrac opportunities, $680MM of 2025 CAPEX (57% of company total).

------ Deal History: Entered 2014 with $2.6B NonOp buy from Aurora Oil & Gas, now 25% WI under COP in Karnes Trough Area. In 2023, paid $2.5B for Ranger Oil establishing operations and gaining 53,000 BOEPD.

------ US v. Canada: Baytex's Eagle Ford operations account for 55% of total free cash flow and 57% of production.

------ Canada Base: Heavy oil in Peace River, Peavine, Lloydminster produces 44,000 BOEPD. Light oil in Viking (legacy) and Duvernay (growth) producing 18,000 BOEPD. Figures are 2025 full year estimates.

Here are our quick takeaways from our report along w/ two slides.

Quick Quotes:

------- Is it all about Canada? "Baytex has an exceptional resource just NW of Red Deer in Alberta in the Pembina Duvernay play. In 2Q, the play averaged 6,667 BOEPD (80% liq.) on the back of a record 3-well pad that avg. IP30/well of 1,865 BOEPD (66% oil, 23% NGL). It owns 140 net sections that could be a growth engine."

------- Content: “We rank and map the top 15 Eagle Ford operators (>85% of total volumes), provide a history of Eagle Ford deals >$100MM since May 2019, and graph total Eagle Ford oil and gas volumes since 2014."

------- Contrast: “Baytex's recent record success in its Pembina Duvernay play may be driving a potential Eagle Ford exit its Canadian assets may have a longer runway and better economics.”

------- Context: “An Eagle Ford exit would shrink Baytex's cash flow and volumes by more than half, although it would also return the company to a pure-play Canadian E&P and likely provide for more strategic options within Canada."

#1---

Here's an Overview

#2---

Here's our Insight & Intel on the Deal

The FULL 7-page report is available for download to the right.

Energy Advisors Group is working hard to expand our thought leadership leveraging our decades of industry expertise. We look forward to providing additional market insight for our clients through Market Monitor, Regional Perspectives, Deal Alerts and Quarterly M&A Outlook.

Our firm has been serving the needs of buyers, sellers and capital providers for over thirty-five years. We stand ready to assist asset owners in a competitive divestment process and to help buyers find off-market strategic assets for their portfolio. Call Rich Martin at 214-744-2495 or email rmartin@energyadvisors.com for a private consultation.

TO LEARN MORE:

Blake Dornak

Vice President

Phone: 713-600-0169

– Email: bdornak@energyadvisors.com

Brian Lidsky

Director-Research & Special Projects

Phone: 713-600-0138

– Email: blidsky@energyadvisors.com

IF YOU NEED ASSISTANCE downloading the full report or creating a login into our platform , contact:

Stephanie Epps

– Email: stephanie@energyadvisors.com

This article is for informational purposes only and not intended as financial advice. Please conduct your own research before investing.