04Q25 QUARTERLY M&A REPORT

Research/Study

All Standard Disclaimers Apply & Seller Rights Retained

DEAL PERSPECTIVES (MEDIA VERSION)

Quick 10 Pages Of The Full 28 Page Report

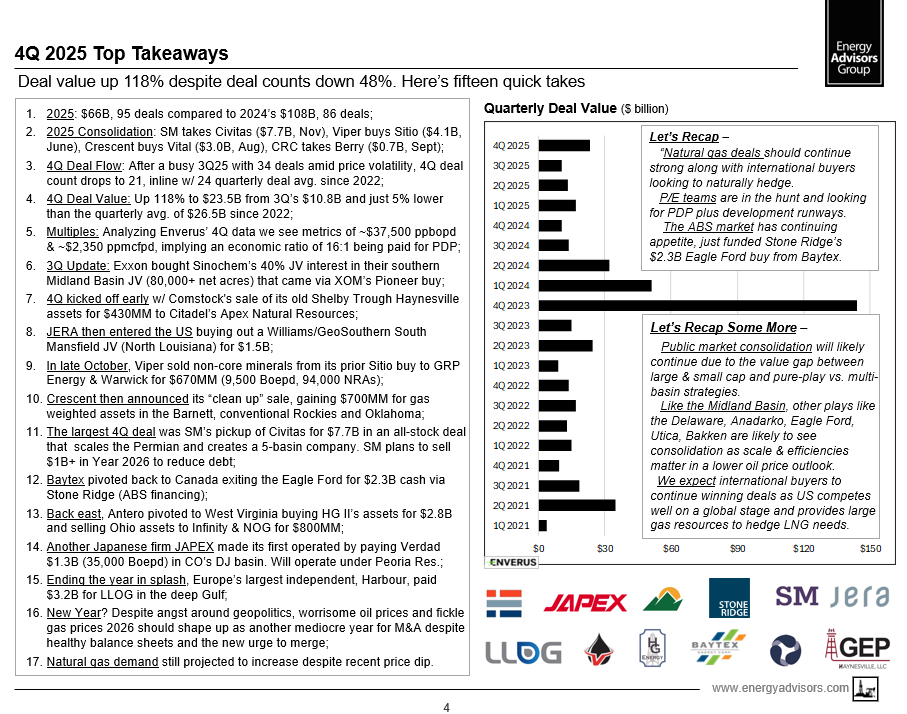

$23.5B IN 4Q25 - UP FROM $10.8B IN 3Q

Deals Decrease To 21 From 34 In 3Q

Close to the 24 Deals/Qtr Avg. Since 2022

SM buys Civitas Via Merger For $7.7B

Harbour Enters Gulf of America For $3.2B

Stone Ridge Buys Baytex's EF For $2.3B

JERA Buys Haynesville For $1.5B

JAPEX Starts Ops In DJ For $1.3B

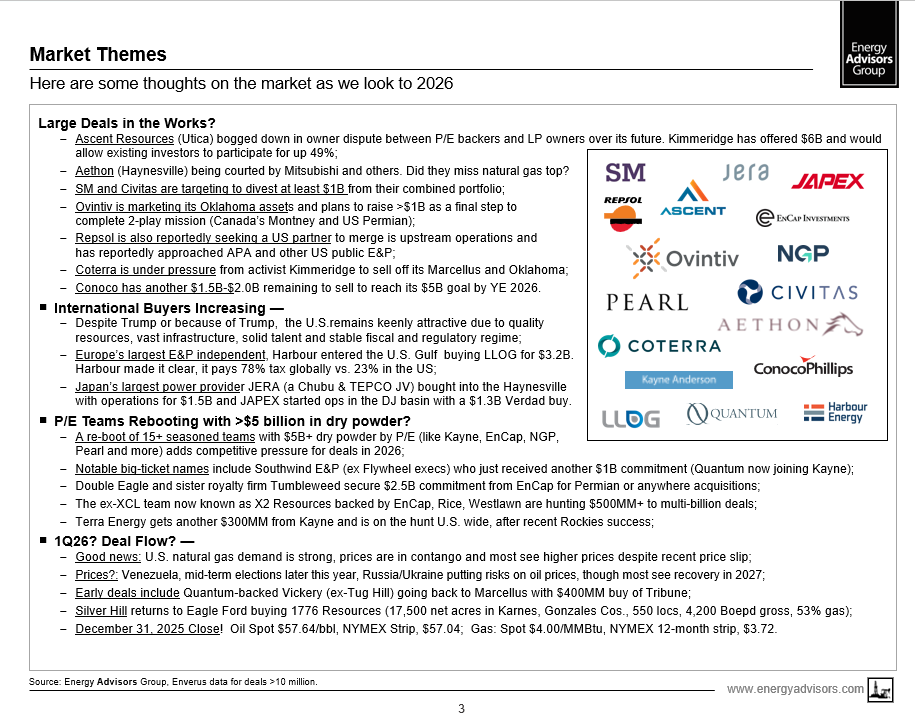

P/E Hunting With 15+ Teams And >$5B

International Buyers Increasingly Active

Consolidation Continuing

Big Deals Underway in HV, OK, Appalachia

Oil Prices Create Angst, Gas Stronger

CONTACT EAG FOR FULL 28 PAGE REPORT

RS 2523MA

THIS IS THE ABBREVIATED MEDIA VERSION

Energy Advisors Group has released a 4Q 2025 Special Report on the U.S. A&D marketplace as a continuation of our Market Monitor Series and thought leadership efforts. The full 28-page Special Report provides perspectives on the outlook plus past and current trends in deal values, counts, plays and valuations.

Our firm has over 35 years of experience assisting clients navigate the marketplace to maximize their portfolios as advisors on both the sell and buy side. Energy Advisors also provides consulting services including asset management and optimization.

Here are our quick quotes, and current market themes from our report.

Quick Quotes:

------- How was 2025? "Publicly reported transactions slowed to $66B, down from $108B in 2024. Deal counts however increased to 95 from 84 in 2024. Public E&P consolidation continued with SM taking Civitas ($7.7B, Nov), Viper buying Sitio ($4.1B,June), Crescent getting Vital ($3.0B, Aug) and CRC buying Berry ($0.7B, Sept)."

------- How was the fourth quarter? "Publicly reported transactions rebounded in 4Q25 to $23.5B from $10.8B prior quarter. However, deal counts lower at 21 from 34."

------- Metrics: "Current economic ratio of 16:1 with market multiples of $37,500 ppbo/d and $2,350 ppmcf/d.”

------- Globally: "Upstream, 4Q25 was $30.8B, up from $18.7B. US share 76%, Canada 13% and International 11%."

Market Themes:

------- Buying Expands Beyond Permian. Since 2022, pure-play Permian deal flow drove 40% of of the U.S. market as majors and large independents consolidated interests. In 4Q, the share accounted for <10% as buyers shifted their focus to Appalachia, Rockies & Gulf.

------- Natural Gas Gaining Momentum. Pure-play gas deals were 28% of transactions in 4Q25 compared ~11% historically. Four of the top 10 deals are natural gas, including Marcellus, Haynesville and Barnett.

------- Private Equity Firms Are Hunting. We are tracking more than 15 teams armed with over $5B in dry powder looking across the U.S to re-boot. Major sponsors include Quantum, Kayne, NGP, EnCap, Rice and Pearl.

------- International Interest. The US is attractive due to resources, infrastructure attractive regulatory and fiscal regimes. In 4Q, UK's Harbour entered the US Gulf w/$3.2B acquisition of LLOG while Japan's JERA and JAPEX bought operated assets in the Haynesville and DJ, respectively."

------- Large Deals Coming?. Ascent should sell, but has been bogged down in an owner dispute, but Kimmeridge has bid $6B. Aethon (Haynesville) is rumored to be of interest to Mitsubishi while Ovintiv is marketing its Oklahoma assets ConocoPhillips still has $1.5-$2.0 billion on its $5.0 billion YE26 sale target.

------- Competitive Market Despite Crude Price Worry. While geopolitics create uncertainty surrounding global oil flows and prices, domestic natural gas remains bullish.

------- Minerals and NonOp Have Solid Competition. A continuing theme across all deal sizes as investors drawn to attractive yields and pricing upside and investments needing minimal G&A and operational necessities.

------- Consolidation Plays. The valuation gap between large cap and small cap public E&Ps facilitates more consolidation. While Midland Basin is largely locked up, other areas like the Delaware, Eagle Ford, Utica, Bakken and Anadarko all have substantial running room for more deals.

------- Power. Some believe that the uplift in power needs from natural gas is not fully reflected in the forward markets. Supermajors, E&Ps and midstream companies are all purposely gaining more exposure higher-growth power demand.

#1---

Here is additional insight from the report taken from one of our slides:

#2---

Here's Quarterly Takeaways and Quick Outlook:

#3---

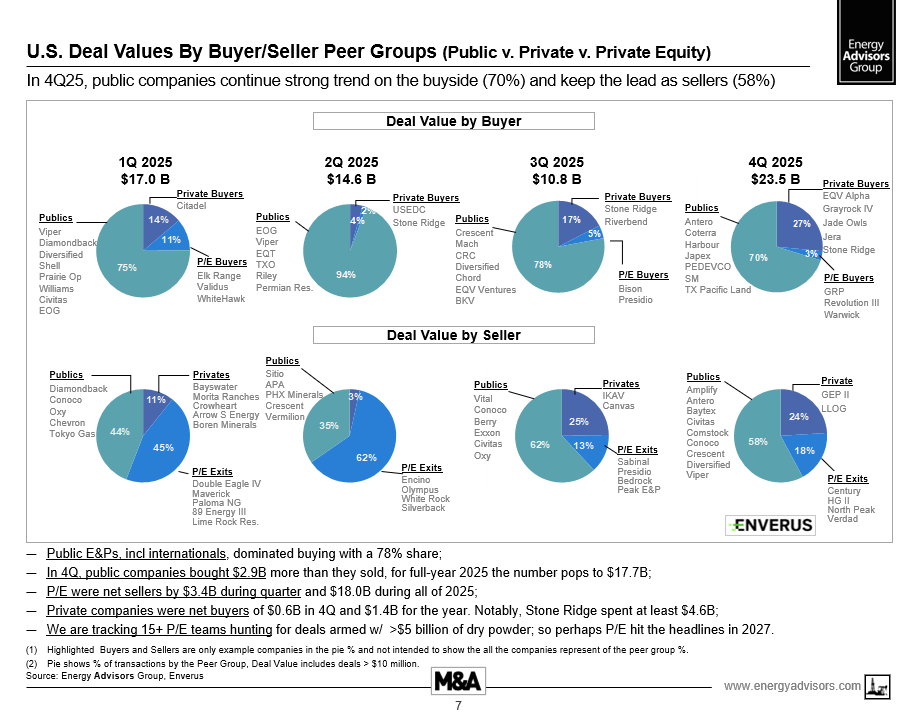

Here is a striking slide demonstrating public companies dominating the buyside:

The 10-page media report is available to the right.

Interested parties desiring to see the entire 28 page report should email any one of us down below for the complete version.

Energy Advisors Group is working hard to expand our thought leadership and look forward to providing additional market insight for our clients through regional perspectives, M&A analysis and market monitor.

Our firm has been serving the needs of buyers, sellers and capital providers for over thirty-five years.

TO LEARN MORE AND RECIEVE A COPY OF THE FULL REPORT CONTACT :

Blake Dornak

Vice President

Phone: 713-600-0169

– Email: [email protected]

Brian Lidsky

Director

Phone: 713-600-0138

– Email: [email protected]

Corporate Office:

4265 San Felipe Ste 650

Houston TX 77027

Corporate Switchboard: 713-600-0123

DEAL PERSPECTIVES (MEDIA VERSION)

Quick 10 Pages Of The Full 28 Page Report

$23.5B IN 4Q25 - UP FROM $10.8B IN 3Q

Deals Decrease To 21 From 34 In 3Q

Close to the 24 Deals/Qtr Avg. Since 2022

SM buys Civitas Via Merger For $7.7B

Harbour Enters Gulf of America For $3.2B

Stone Ridge Buys Baytex's EF For $2.3B

JERA Buys Haynesville For $1.5B

JAPEX Starts Ops In DJ For $1.3B

P/E Hunting With 15+ Teams And >$5B

International Buyers Increasingly Active

Consolidation Continuing

Big Deals Underway in HV, OK, Appalachia

Oil Prices Create Angst, Gas Stronger

CONTACT EAG FOR FULL 28 PAGE REPORT

RS 2523MA

THIS IS THE ABBREVIATED MEDIA VERSION

Energy Advisors Group has released a 4Q 2025 Special Report on the U.S. A&D marketplace as a continuation of our Market Monitor Series and thought leadership efforts. The full 28-page Special Report provides perspectives on the outlook plus past and current trends in deal values, counts, plays and valuations.

Our firm has over 35 years of experience assisting clients navigate the marketplace to maximize their portfolios as advisors on both the sell and buy side. Energy Advisors also provides consulting services including asset management and optimization.

Here are our quick quotes, and current market themes from our report.

Quick Quotes:

------- How was 2025? "Publicly reported transactions slowed to $66B, down from $108B in 2024. Deal counts however increased to 95 from 84 in 2024. Public E&P consolidation continued with SM taking Civitas ($7.7B, Nov), Viper buying Sitio ($4.1B,June), Crescent getting Vital ($3.0B, Aug) and CRC buying Berry ($0.7B, Sept)."

------- How was the fourth quarter? "Publicly reported transactions rebounded in 4Q25 to $23.5B from $10.8B prior quarter. However, deal counts lower at 21 from 34."

------- Metrics: "Current economic ratio of 16:1 with market multiples of $37,500 ppbo/d and $2,350 ppmcf/d.”

------- Globally: "Upstream, 4Q25 was $30.8B, up from $18.7B. US share 76%, Canada 13% and International 11%."

Market Themes:

------- Buying Expands Beyond Permian. Since 2022, pure-play Permian deal flow drove 40% of of the U.S. market as majors and large independents consolidated interests. In 4Q, the share accounted for <10% as buyers shifted their focus to Appalachia, Rockies & Gulf.

------- Natural Gas Gaining Momentum. Pure-play gas deals were 28% of transactions in 4Q25 compared ~11% historically. Four of the top 10 deals are natural gas, including Marcellus, Haynesville and Barnett.

------- Private Equity Firms Are Hunting. We are tracking more than 15 teams armed with over $5B in dry powder looking across the U.S to re-boot. Major sponsors include Quantum, Kayne, NGP, EnCap, Rice and Pearl.

------- International Interest. The US is attractive due to resources, infrastructure attractive regulatory and fiscal regimes. In 4Q, UK's Harbour entered the US Gulf w/$3.2B acquisition of LLOG while Japan's JERA and JAPEX bought operated assets in the Haynesville and DJ, respectively."

------- Large Deals Coming?. Ascent should sell, but has been bogged down in an owner dispute, but Kimmeridge has bid $6B. Aethon (Haynesville) is rumored to be of interest to Mitsubishi while Ovintiv is marketing its Oklahoma assets ConocoPhillips still has $1.5-$2.0 billion on its $5.0 billion YE26 sale target.

------- Competitive Market Despite Crude Price Worry. While geopolitics create uncertainty surrounding global oil flows and prices, domestic natural gas remains bullish.

------- Minerals and NonOp Have Solid Competition. A continuing theme across all deal sizes as investors drawn to attractive yields and pricing upside and investments needing minimal G&A and operational necessities.

------- Consolidation Plays. The valuation gap between large cap and small cap public E&Ps facilitates more consolidation. While Midland Basin is largely locked up, other areas like the Delaware, Eagle Ford, Utica, Bakken and Anadarko all have substantial running room for more deals.

------- Power. Some believe that the uplift in power needs from natural gas is not fully reflected in the forward markets. Supermajors, E&Ps and midstream companies are all purposely gaining more exposure higher-growth power demand.

#1---

Here is additional insight from the report taken from one of our slides:

#2---

Here's Quarterly Takeaways and Quick Outlook:

#3---

Here is a striking slide demonstrating public companies dominating the buyside:

The 10-page media report is available to the right.

Interested parties desiring to see the entire 28 page report should email any one of us down below for the complete version.

Energy Advisors Group is working hard to expand our thought leadership and look forward to providing additional market insight for our clients through regional perspectives, M&A analysis and market monitor.

Our firm has been serving the needs of buyers, sellers and capital providers for over thirty-five years.

TO LEARN MORE AND RECIEVE A COPY OF THE FULL REPORT CONTACT :

Blake Dornak

Vice President

Phone: 713-600-0169

– Email: [email protected]

Brian Lidsky

Director

Phone: 713-600-0138

– Email: [email protected]

Corporate Office:

4265 San Felipe Ste 650

Houston TX 77027

Corporate Switchboard: 713-600-0123